Our family pays thousands annually for insurance–pretty sour! Lemonade’s slick website and app promises “incredible” pricing and provides a direct way to quote and purchase home and car insurance. Can my lemons be made into lemonade?

Lemonade’s theory is that by using AI instead of local insurance agents at almost every phase of insurance it can save us money.

Lemonade promises fast insurance with “awesome” prices . . . so why not see how their process works and see if I could save some money? Hey, everyone has their price!

After all, our family shelled out about $6,200 this year for our home, auto, and earthquake policies. That’s to insure a creaky home, four older cars, and six good drivers who range through Hillsboro and Beaverton daily and to wider areas like North Plains, Forest Grove, or Portland monthly.

Because I am an independent insurance agent, I can check insurance rates with multiple carriers and also have a good sense of coverages. It also means we don’t have minimal policies since I see value in many of the options that insurers offer.

So how did it go? If you don’t care about my comments on the shopping experience at Lemonade, you can skip to the pricing results below.

Note – Since I am an independent insurance agent, Lemonade is our competitor in one way with similar products. In another, they’re not since our clients differ markedly. Clients of Sensible Insurance PNW of course value competitive pricing, and our clients also tend to value genuine human interaction and thoughtful feedback on their insurance choices. Lemonade seems to be targeting people who want awesome pricing, know little about insurance, and avoid human interaction.

How About The Home Shopping Experience:

I was a bit surprised to see them promise an “awesome bundle price” since, with the way insurance rates work, you actually don’t know if the price is “awesome” until after you’ve done the quote.

But anyways, of course I’m open to an awesome price!

Lemonade said it was gathering info on my home from data sources. This isn’t crazy since information about our home is listed online along with fairly accurate description: a daylight ranch.

Lemonade didn’t know if it was a mobile home and then said “It looks like you live in a Cape Cod style home.” Ummm, nope; so I fixed it quick. Then it asked the year built, so I entered the year (which I’d think would be the most available piece of info online), and it got the countertops wrong, which I fixed. It’s not crazy that it got some of this info wrong, but it is strange how confidently wrong it was.

The Home Coverages:

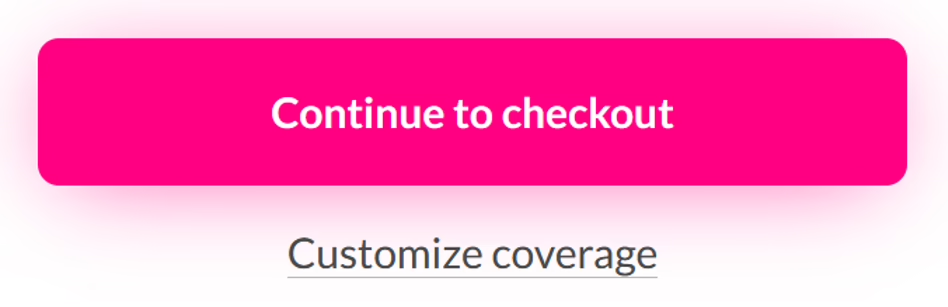

The coverages page was a nightmare waiting to happen. I say “waiting to happen” because each page is clearly designed to speed me to the checkout without looking at or reviewing the coverages. The bright pink button above appears at the top of the page before you even see coverages. (See dark pattern: “misdirection” at Wikipedia.)

The default coverages were wonky. And let me say first here, I think default coverages in quoting are fine. Every seller has to propose some initial variety of product, but in this situation, where they’re trying to move you along quickly, the default coverages become even more important. Why? Because there’s a good chance a client may not even view the coverage.

So what were the defaults?

The standard deductible option was $500 or $1,000. Not only is this low for an Oregon home policy, there also was no option to go higher except for wind/hail losses. What’s perplexing about this is that higher deductibles are a key way of keeping the insurance costs down. (Note- When I reopened the quote days later, the standard deductible options went up to $2,500).

The roof defaulted to Actual Cash Value instead of Replacement Cost. In other words, any roof claim would be depreciated based on age. Unless you already have an older roof, that’s an unusual starting point.

It excluded Building Code coverage. Strange again. Nearly all competitors include at least 10% by default and this could result in major problems for a client with a significant home claim. For instance, my own home, built over 50 years ago, would need some code updates. Under Lemonade’s default, there is no provision for such expenses.

It included over $500k of personal property coverage, which is way high for my situation in Oregon. So I bumped it down.

It did not include earthquake coverage. This is okay since some people choose not to purchase this, but when I did toggle to add earthquake coverage the system doesn’t tell me any details about the actual earthquake coverage. This is unhelpful because it matters. Earthquake deductibles in Oregon can range from 5% up to 25%. What am I purchasing?

It only offers up to $5000 for Water Backup. This is more typical of a renter’s than a homeowner’s policy.

It does not offer any sort of Hidden Water or Water Seepage option. This matters for claims involving longer term hidden leaks, which are usually not covered under standard policy contracts.

How About The Car Insurance Process?

After spending ten minutes on my home quote, Lemonade began my car quote by asking for my home address. Odd. I just gave them that.

It nicely pulled up my four vehicles and drivers correctly. Filling out the driver info was a bit tedious but to be expected with six drivers.

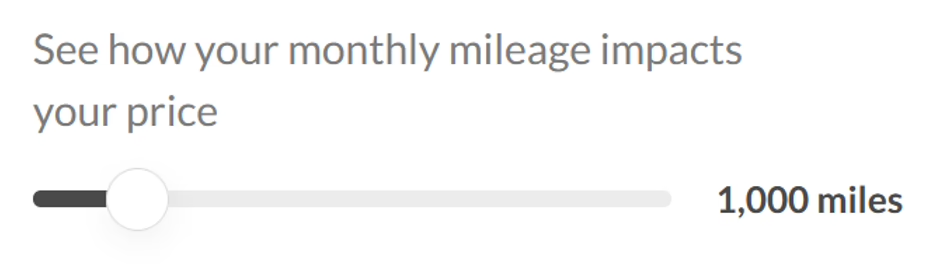

Lemonade bragged about saving money with their mileage-based rate. I like the concept! And they have a cool slider bar, though it is unclear whether the slider is asking for all my vehicles or just one.

Again, Lemonade asks me to checkout before even reviewing the coverage on the policy.

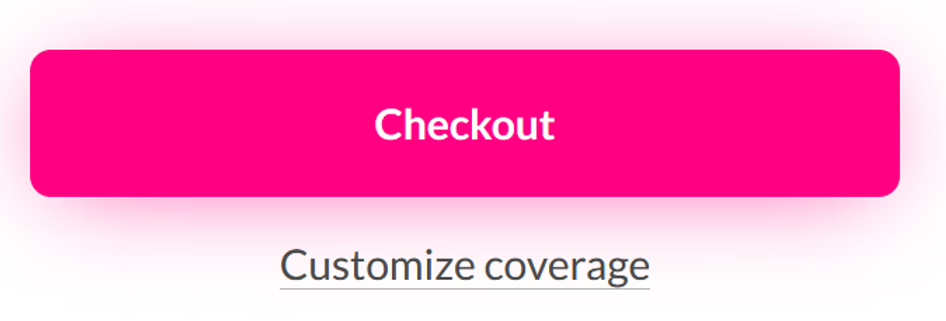

What happens when I click “Customize coverage”?

I discover that the quote matches my current liability limits. That’s nice.

BUT again, the defaults are bad.

It defaulted to not having damage coverage on any of my vehicles. In other words, if I had just clicked “Checkout” and bought the policy, I would have liability only and damages to my vehicles would not be covered. Seems important.

There’s also no option to increase my personal injury protection from $15k to my current $25k. This is not a huge deal since in Oregon most people go with the $15k, but still, not even an option.

Oh, and I do see that I can adjust the mileage per car further along. When I adjust the mileage to be more accurate, it does improve my price. Nice.

How Did Pricing Turnout at Lemonade?

If I went with Lemonade for my home and car insurance I’d pay more than double, about 150% more per year– $9,500 more! Incredible in one way, I guess.

Home insurance? My current is $1795 annual including our earthquake policy versus Lemonade’s $3708, which includes earthquake but weaker coverage overall.

Car insurance? My current is $4,402 annual versus Lemonade’s $12,060. That’s for similar coverages though less policy benefits.

(Note – Lemonade does change pricing monthly based on mileage, so the cost might end up somewhat lower or higher if my estimates are off. If we drove each vehicle only 50 miles per month, Lemonade’s cost would be about the same. But, considering we live in suburban Aloha, Beaverton, and Hillsboro with family activities all over the metropolitan area, driving so few miles is for now a dream.)

Final Thoughts:

It’s important to remember that our family is only one household in the Hillsboro area. I wouldn’t be surprised if Lemonade gives a better rate to other situations with how insurance rates work. After all, most insurers build their products and focus their pricing for certain market segments. Maybe someone with one car and a newer house or a renter would do better? So it doesn’t bother me that Lemonade might offer–even wildly–different rates for different situations.

What does bother me is that Lemonade seems designed to take advantage of people’s ignorance.

Lemonade declares “incredible” prices and a bundle price that is “awesome” without knowing if it will be either. (See my observations on insurtech/fintech lingo here.)

More troubling, Lemonade’s process seems designed to win people who are in a rush and know little about insurance. This can end badly.

If I had gone with Lemonade’s default selections, my vehicles wouldn’t be covered for damage, my roof wouldn’t have replacement cost, and my home would be missing coverages that are near industry standard among other things.

Because this is by design, I can’t help but wonder if this will make Lemonade a target in future lawsuits. Sure, this design may reduce someone’s cost and momentarily win Lemonade more sales, but in the long run, it seems likely to leave clients without important coverages. That will matter when claims happen. And I’m fairly certain the attorneys will not forget everything they know about insurance.

TL;DR

My experience, having several cars, good drivers, and a 50 year-old home here in Oregon, is that getting a direct quote through Lemonade resulted in way higher insurance premiums than I currently have and, if I weren’t an insurance agent, would likely leave me with major coverage shortfalls.

Want a thoughtful comparison for your auto, home, and personal liability umbrella? Give us a call or email us. We’d love to help.

Learn more About Us (actual people!), our Sensible Approach, or our Carriers.